Peak Uncertainty May Be Behind Us. Here is What the Data Says.

Published

Happy Friday. We’re about four weeks into the Iran conflict, and something feels like it’s starting to shift. Even it is on the edge. Our view is we’ve probably hit peak uncertainty around war. That doesn’t mean this ends tomorrow, and it won’t be a straight line. But when you step back, the incentives are starting to lean more toward resolution than escalation.

Start with domestic politics. Republicans heading into midterms with elevated gas prices just doesn’t work. Every extra week of disruption in Hormuz adds pressure. Then look at who’s actually feeling the impact. It’s not just the US. Japan, South Korea, India… all heavily reliant on those oil flows. Even parts of the Middle East are losing revenue daily if they can’t move crude. Meaning the push for resolution is getting stronger, not weaker.

And then there’s Iran itself. Based on what’s publicly observable, this doesn’t look like something they can stretch out for a long time. So net-net, this feels like we’re starting to move in the right direction. Not clean, not linear, but directionally better. That’s my take.

Also what is interesting is when you zoom out from the headlines, the underlying data still looks pretty constructive. Inflation expectations remain anchored. Consumers are still spending. Job openings are starting to pick back up. Tech insiders are buying their own stock at the highest levels in years. Pension funds have roughly $14B to deploy into equities into quarter-end. Short interest is elevated, which can flip quickly if sentiment shifts. And real rates are coming down, which is supportive even without Fed cuts.

That’s the part that stands out to me.

This Week’s Data

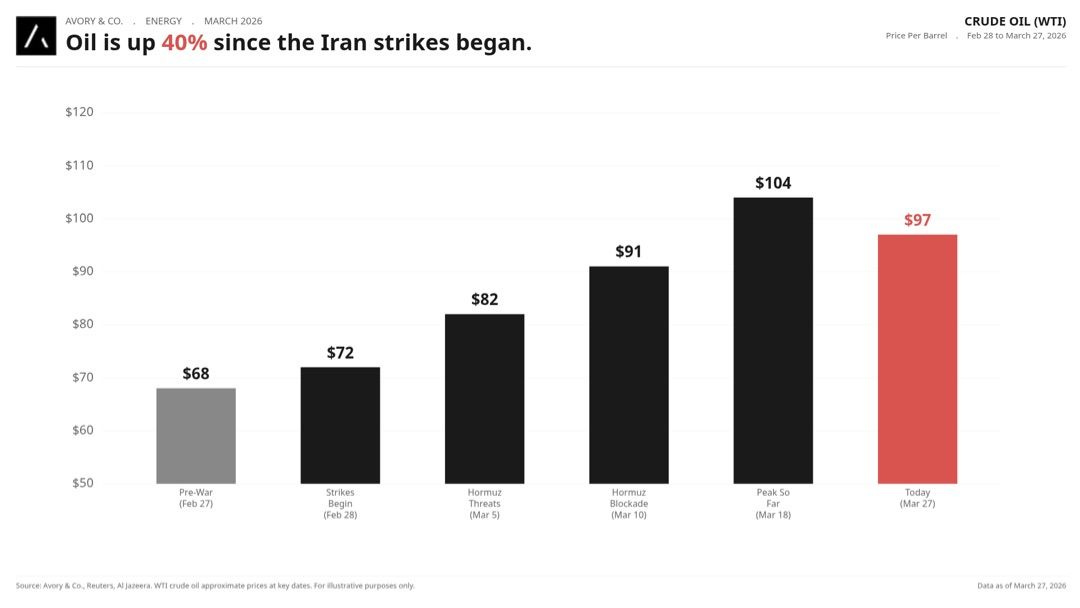

Oil is up 40% since strikes began. But it may have peaked.

WTI went from ~$60 pre-war to a peak of $104 on March 18, and has since pulled back to ~$97. As I’m writing this, it’s moved about $5, so take that as you will heading into the weekend.

The move itself was pretty extreme, +40% in four weeks. But what matters more now is the plateau. Feels like the market is starting to price in some form of resolution, not a prolonged disruption. We may get boots on the ground, but my take on that is that would mean a faster resolution.

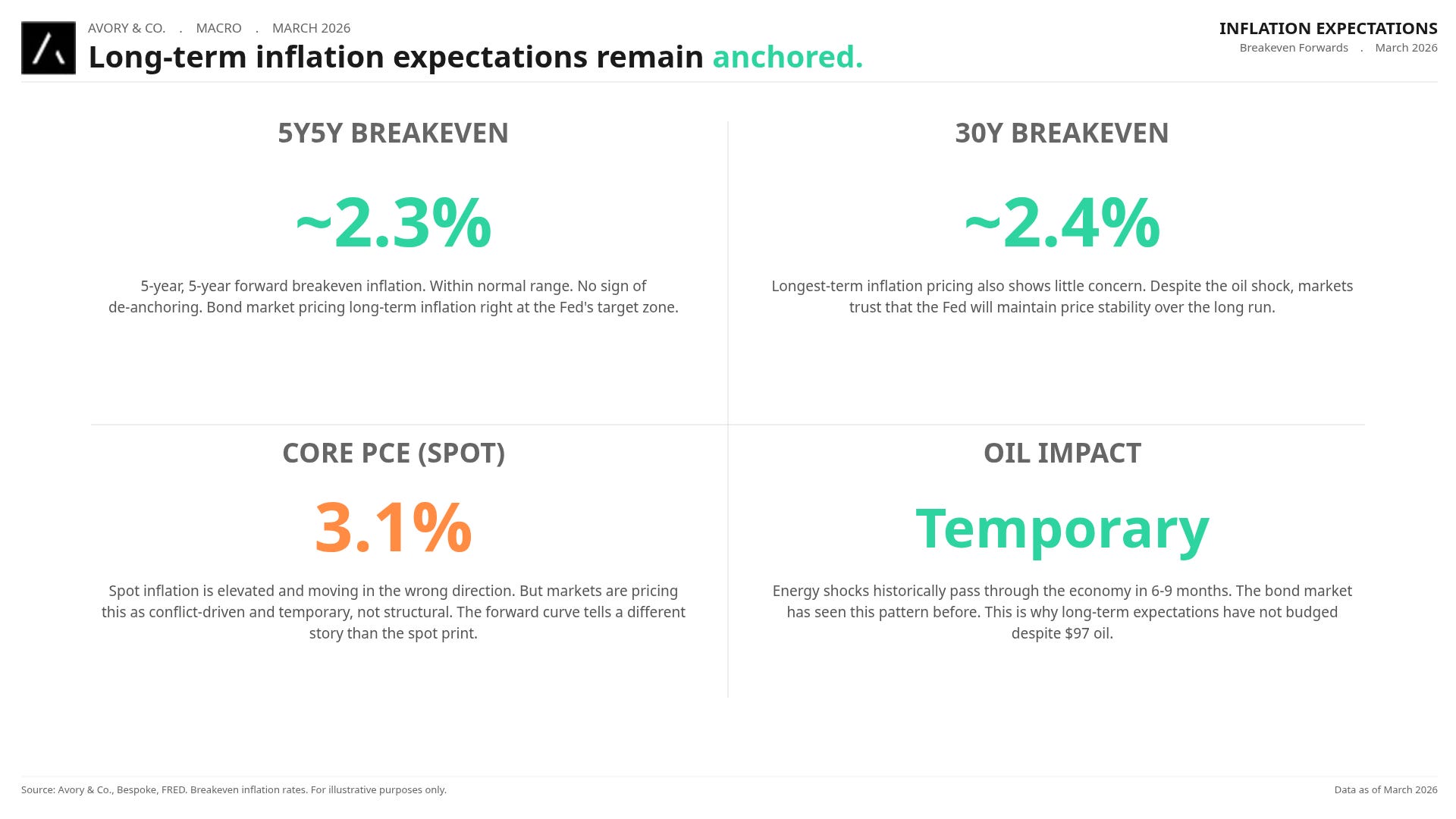

Long-term inflation expectations remain anchored.

The 5-year, 5-year forward breakeven is sitting around 2.3%. The 30-year breakeven is at 2.4%. Neither is showing any sign of de-anchoring. Markets view the inflation impulse as temporary, tied to the conflict, not structural. Historically, energy shock inflation passes through in 6-9 months. The bond market is saying this and we agree.

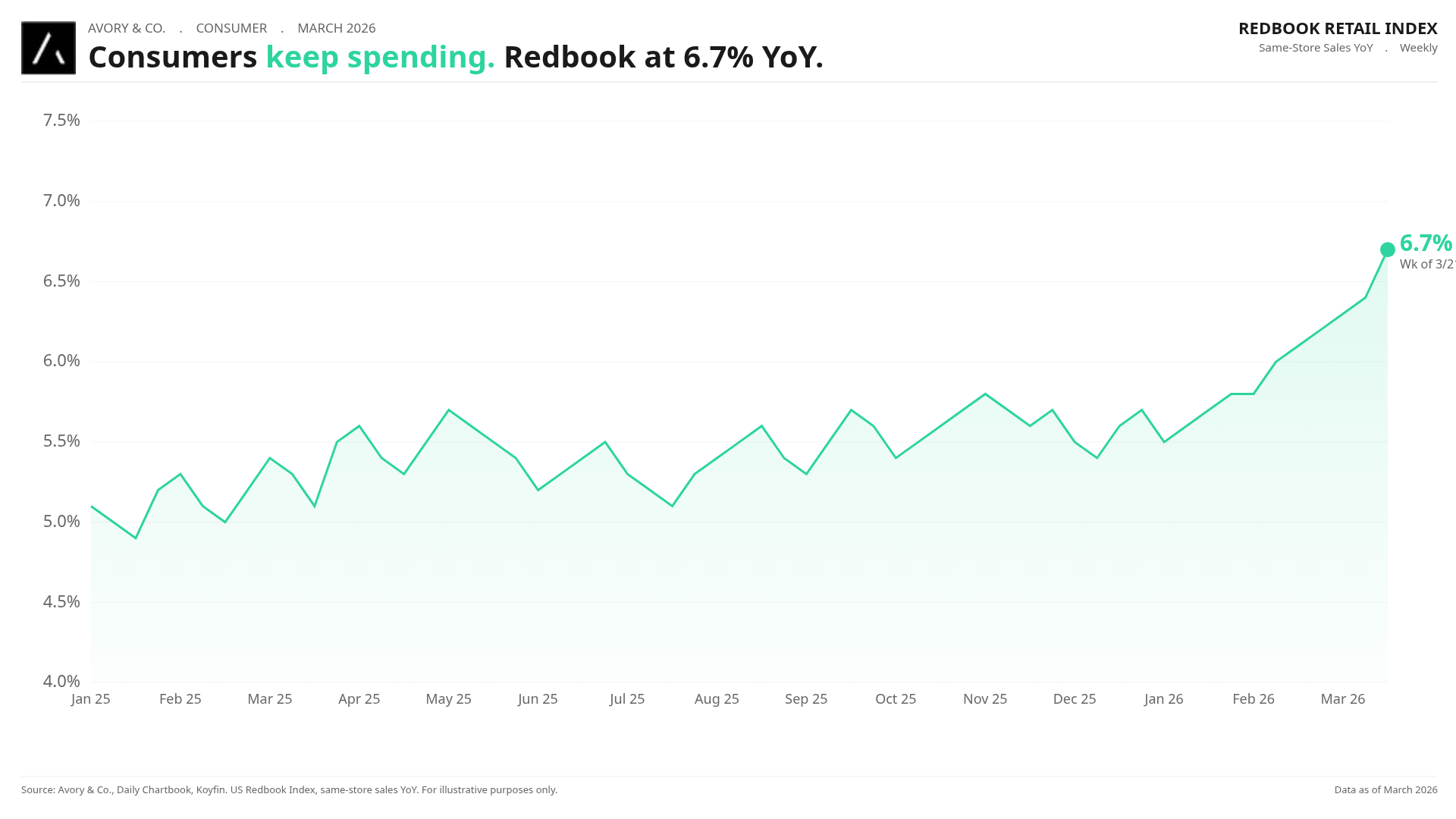

Consumers keep spending. Redbook at 6.7% YoY.

The Redbook Index that measure consumer buying for the week ending March 21 came in at +6.7% YoY, up from 6.4% the prior week. Same-store retail sales are growing even as gas prices rise. Consumer balance sheets are healthier than the headlines suggest it seems.

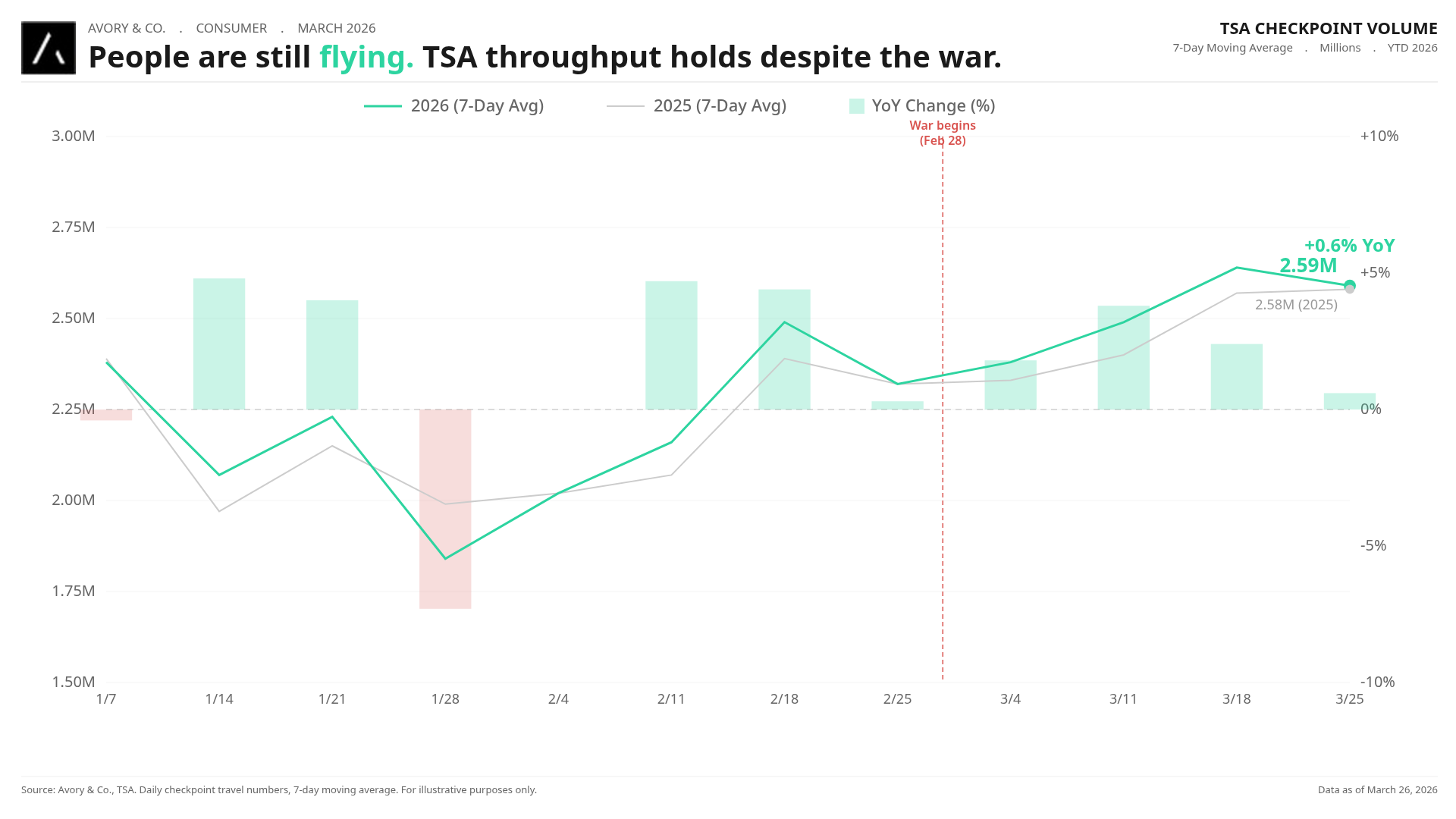

People are still flying. TSA throughput holds despite the war.

TSA checkpoint data through March 26 shows the 7-day moving average at 2.59M passengers, still running +0.6% above the same period in 2025. The consumer is not pulling back on travel.

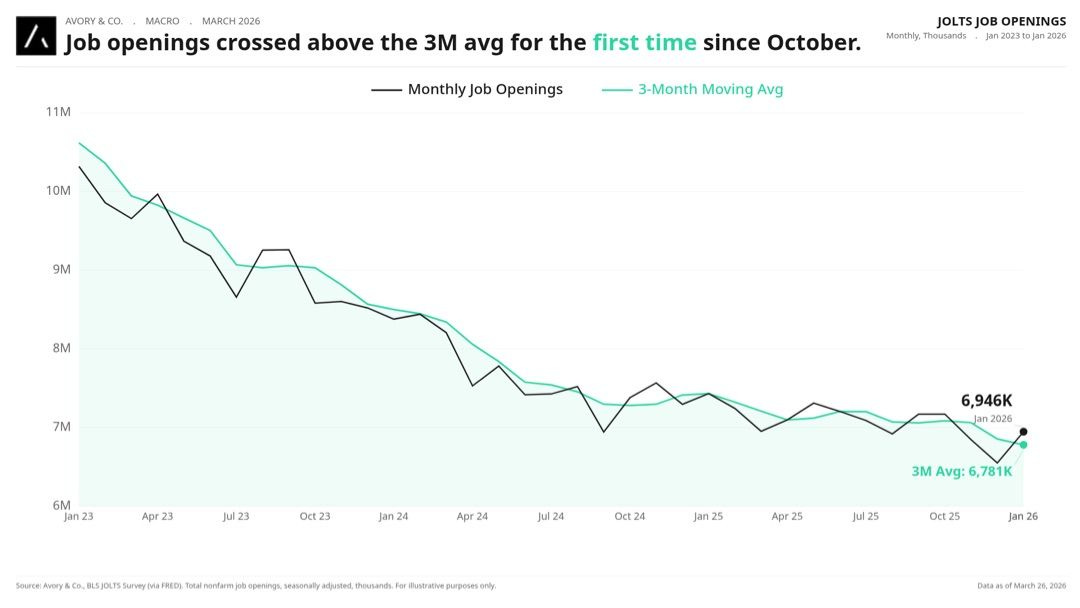

Job openings cross above the 3-month moving average.

JOLTS job openings at 6,946K, pushing above the 3-month moving average for the first time since October 2025. The labor market is stabilizing and potentially inflecting. Lets see.

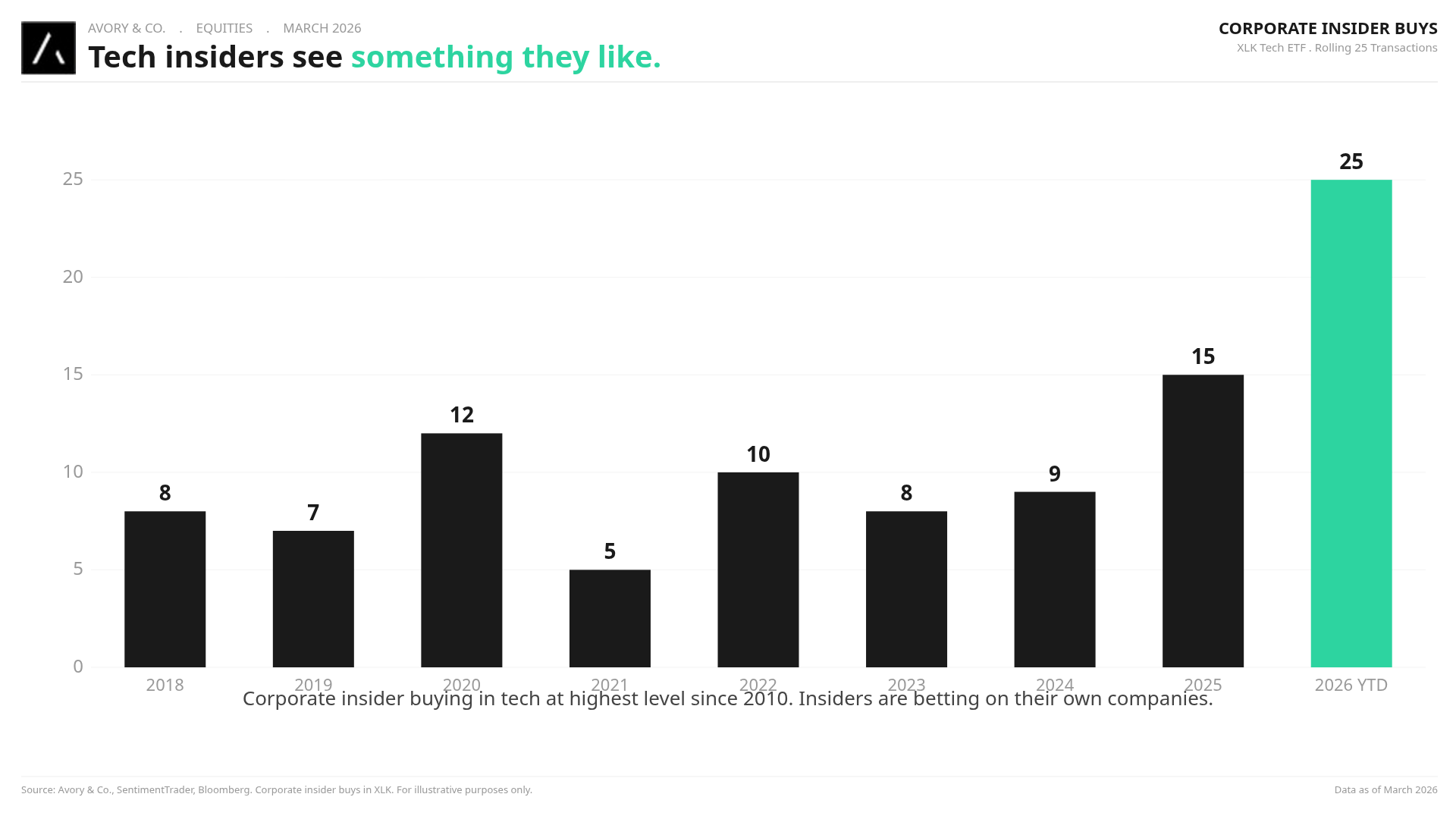

Tech insiders are buying at the highest rate in years.

Corporate insider buys in tech at 25 transactions , highest since 2010. When insiders buy, they are betting their own money. This is skin in the game.

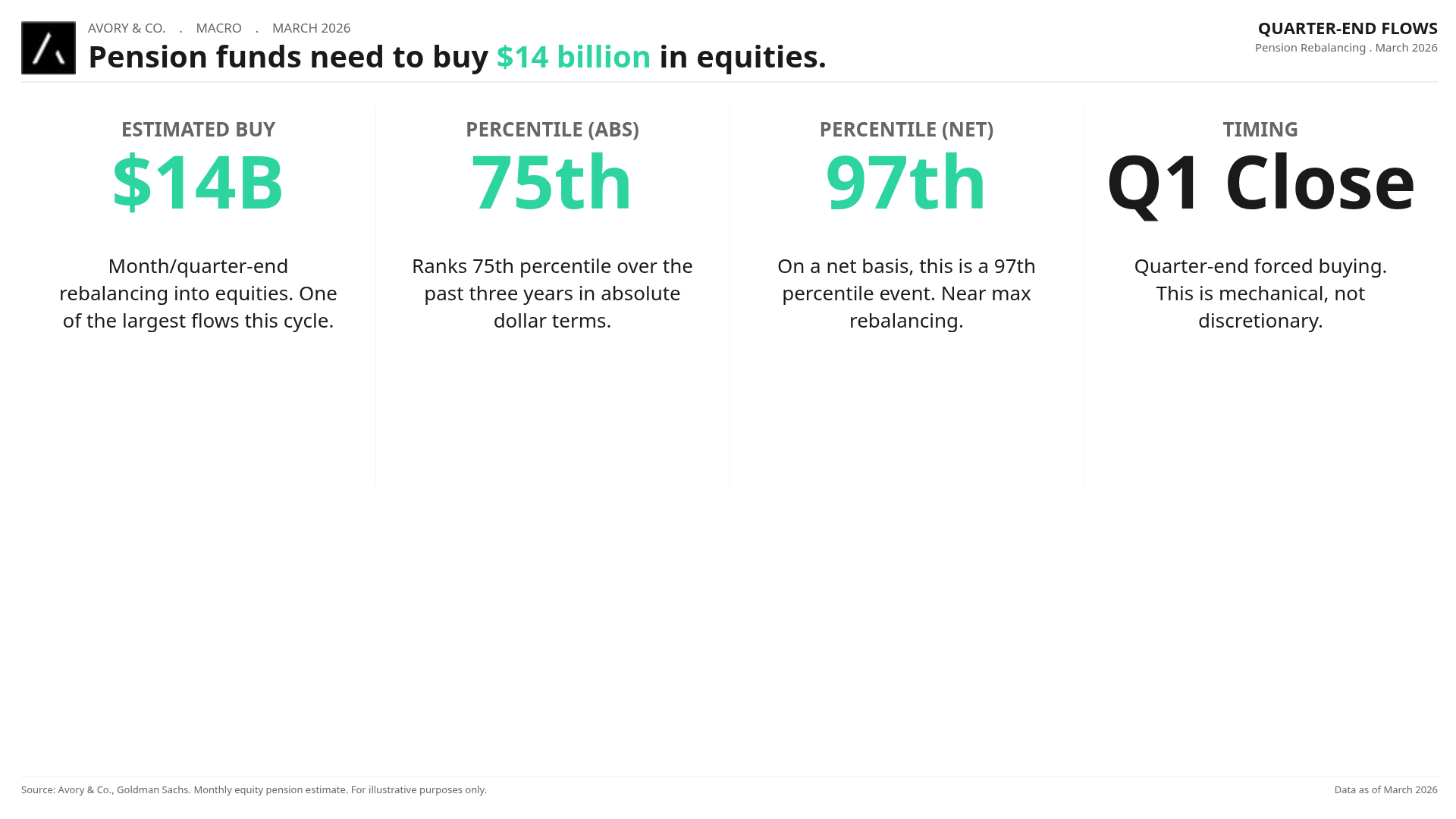

Pension funds need to buy $14 billion in equities.

Goldman Sachs estimates $14B in quarter-end rebalancing. 75th percentile absolute, 97th percentile net. This is mechanical, forced buying heading into Q2. Not a bad setup here.

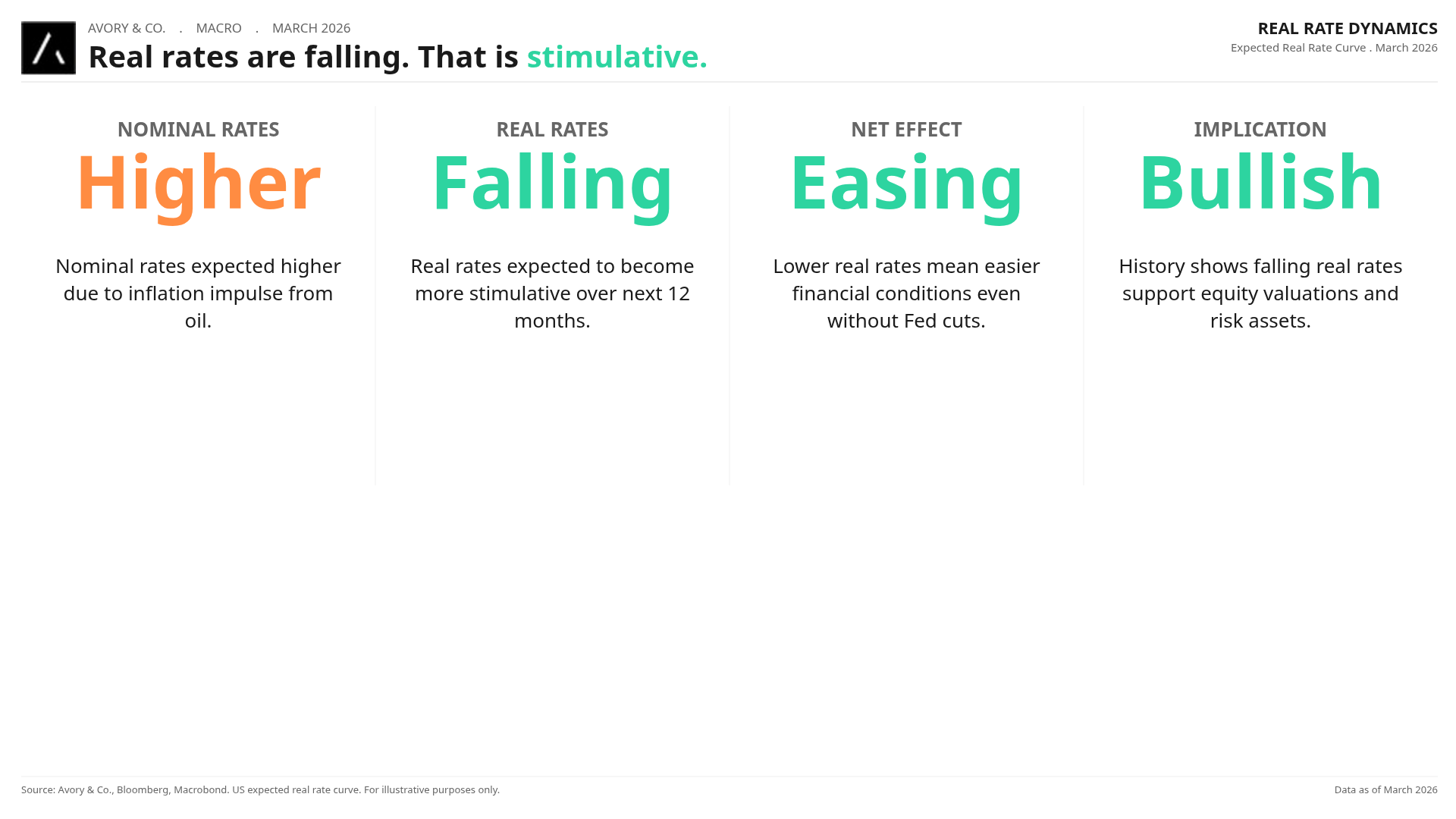

Real rates are falling. That is stimulative.

While nominal rates are expected higher, real rates are falling, making financial conditions more stimulative even without Fed cuts. The inflation impulse is paradoxically making the backdrop more accommodative. Strange how that works.

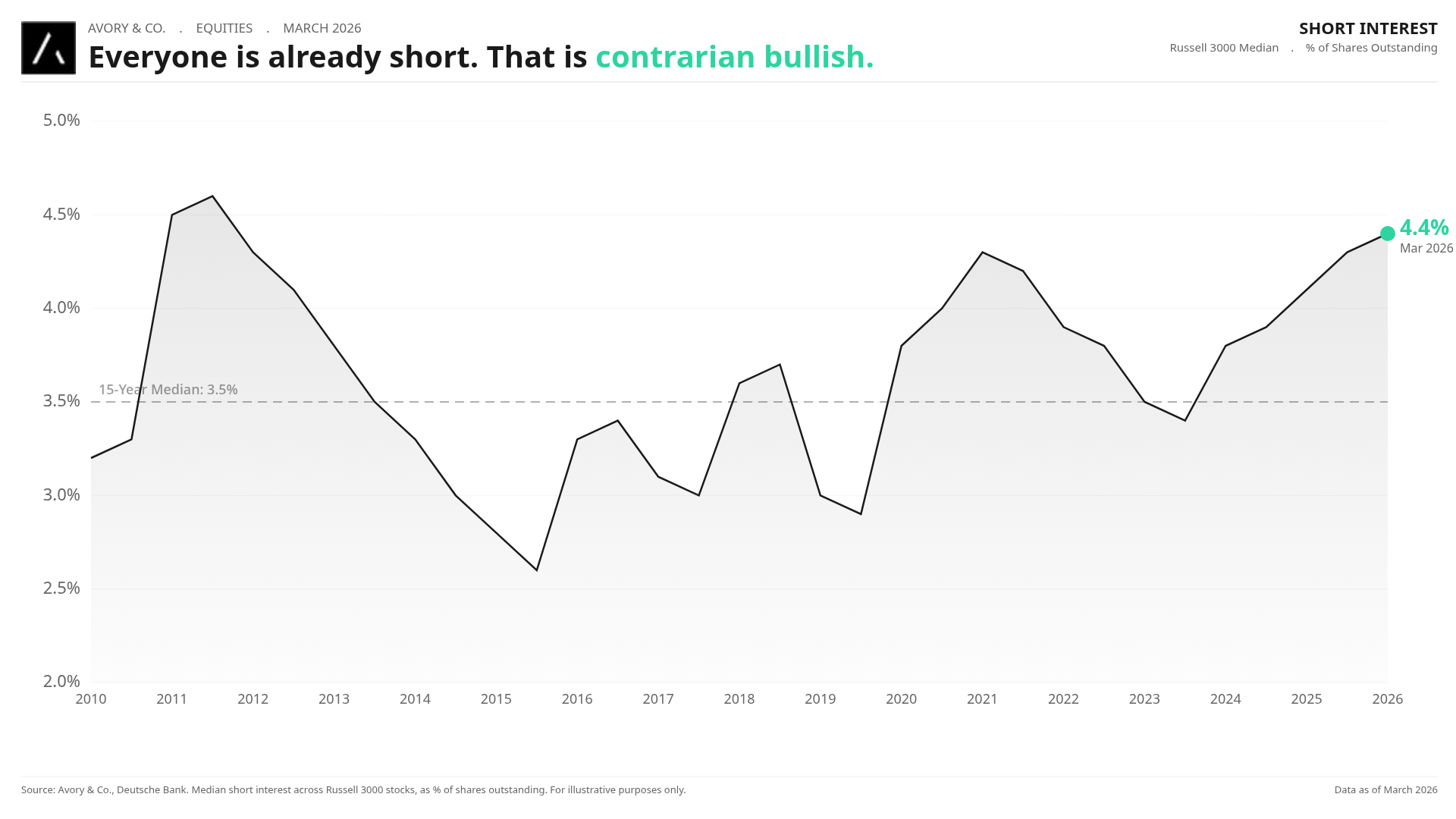

Short interest is already at cycle highs.

Now how about this. When looking at the Russell 3000 median short interest it sits at 4.4%, the highest since 2011. When everyone is already short, the incremental seller is gone. This is a coiled spring. Any positive catalyst forces covering and so like we have seen in the past, moves come fast, so stay the course.

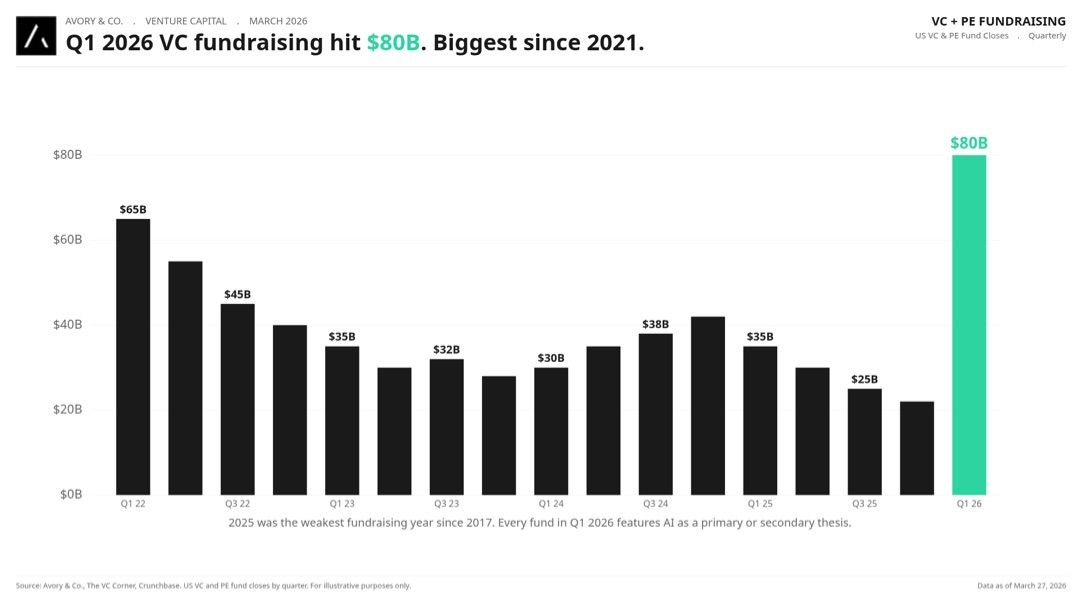

VC fundraising hit $80 billion in Q1. Biggest since 2021.

Now money continues to pour in areas. Q1 2026 fund closes hit $80B, largest since Q1 2022. To me this shows the demand environment.

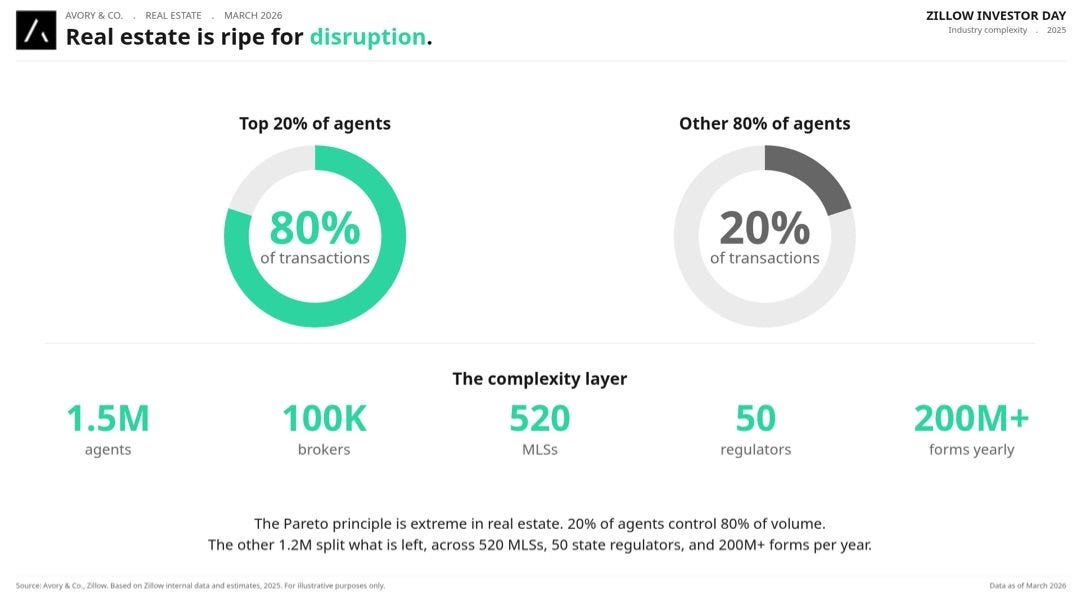

Zillow investor day: AI-native real estate is coming.

Turning to one of our names. Zillow had their investor day and we came away more bullish. AI suite demos, 235M monthly uniques, 80% direct traffic. Once mortgage rates settle, this name could re-rate significantly. But we need to get past the war and concerns on macro first. But they continue to do well and the view of a housing super app is becoming more clear.

Looking Ahead

March jobs report (Friday April 3): The next major data point for the recession debate.

April 9 PCE release: First reading capturing oil-shock price pressures.

Iran conflict: Both sides have signaled willingness to talk. Direction is constructive.

Q1 earnings season: Begins mid-April. We get back to fundamentals!

The data says the world is still moving forward. Peak uncertainty may be behind us. The incentives point toward resolution. And the technical setup, short interest, pension flows, insider buying, falling real rates, is quietly building a case for upside.

Have great weekend!

About Avory & Co.

Investing where the world is headed.

Avory specializes in high-conviction equity strategies, emphasizing Secular Growth and Transformation Stories driven by exceptional teams. Data guides decisions. We cater to high net worth investors, family offices, and institutional investors. Note: This information doesn't constitute a recommendation to buy or sell any mentioned securities. Avory is based in Miami, Florida with clients all across the globe.

Speak to us: Schedule a Brief Zoom Meeting

Send us an email: Team@avoryco.com

Want to invest? We are on most platforms.

Want More

🎥 Avory YouTube Channel

🎙️ Avory Podcast

Disclaimer: Not a recommendation to purchase or sell any securities mentioned. This is for educational purposes only.